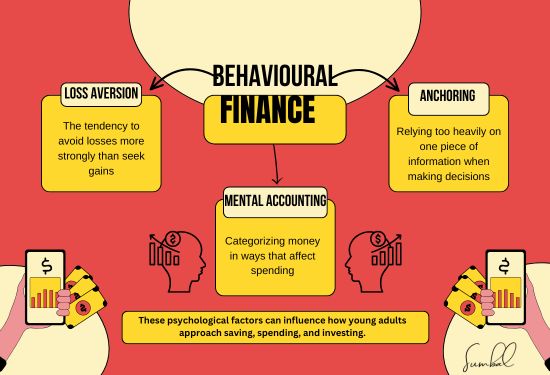

Over recent years, behavioral finance has been used as the main strategy for young adults to develop mindful spending and saving habits. While classical finance theories presuppose that economic agents make rationalized financial decisions, behavioral finance considers that decisions are influenced by biases shaped by emotions and other psychological mechanisms. With this courtesy, financial advisors, apps, and institutions are seeking new approaches to making better money habits, including those of Millennials and Gen Z.

What is Behavioral Finance?

Behavioral finance is an area of study that links psychology with finance in an attempt to explore why people act in financially unreasonable ways despite observing good reasons. For instance, a person may decide to purchase a gadget, knowing very well that this would affect their budget. This field concerns the mental processes or predispositions, feelings, and preferences that influence the decision to buy or invest.

Promoting Mindful Spending Among Young Adults

It is surprising, however, that so many youth are still in high impulse spending, debts, and pressures associated with finances. Behavioral finance can only propose measures to confront these challenges so people develop better attitudes toward spending and saving.

The Power of Defaults

This explains the recent trends of automatic savings, as people are most likely to work with the default value. Digit and Qapital are apps that apply this principle by moving small amounts from checking to savings accounts. This makes saving automatic since the apps assist in developing a saving culture without actively having to remind the user.

Visualizing Goals

Visualization within behavioral finance is the representation of the results in the form of pictures, which is an essential component of the decision-making process. It is easier for individuals to follow the rules laid out by an expert when they achieve financial goals set in the long run. Existing budgeting applications have goal setting where people can enter and be reminded of their savings plans, such as traveling or clearing off a definite college fee balance. For many people, noticing the changes occurring, even if they are small, inspires the adoption of the habit of saving and makes goals achievable.

Using Framing to Encourage Better Decisions

It is clear that how choices are constructed influences decisions. For instance, in a financial application that gives feedback about a user’s saving progress, the positive aspect of saving is focused on rather than the amount spent. This thinking assists in enhancing a sense of mastery or accomplishment that can be leveraged to make better financial decisions.

Tackling Emotional Spending

Impulsive buying is also common among adults due to stress or boredom. Apps like YNAB have the potential to check features that help a user understand where he/she is spending wrongly or unnecessarily. An extreme example is that some sites will use jokes to gently remind users that making impulsive buying decisions is not a good idea, which should make the process less threatening.

Building Financial Habits with Micro-Behaviors

According to many theories on behavioral finance, one can build habits to act in a certain manner and create positive financial behavior through micro-behaviors. That’s why apps that round up your everyday purchases for investment, such as Acorns, use this concept. These small changes enable young adults to save money without any financial planning.

Gold Investing: Safeguarding Wealth with Safe Havens

Mobile Pay Security Pitfalls: How to Keep Payments Safe

Investment Shifts in the AI Revolution

Financial FOMO: Overcoming Social Comparison and Building Sustainable Wealth

Why are index funds appropriate for a new investor?

How Companies Are Changing to Accept Payments in Cryptocurrency

Overseas Assets: Necessity or Luxury?