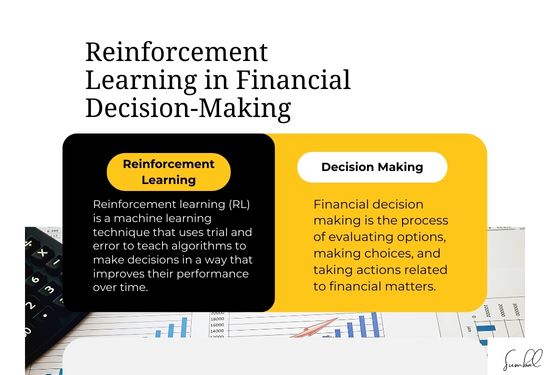

Reinforcement learning (RL), which is a category of machine learning, has become a promising capability in decision-making in financial markets. RL systems maximize plans because they learn from the rewards and do not penalize actions where plans fail. This learning structure resembles the trial-and-error process in human beings. Still, at the super intelligent level of computing, the RL systems can look for and extract profitable trading behaviors. Therefore, reinforcement learning has redefined the financial institution’s trading techniques, investment strategies, and risk management.

Understanding Reinforcement Learning in Finance

Reinforcement learning operates by setting an agent to the environment in the financial market and letting this agent make decisions to accumulate overall pay-offs in the long run. The environment responds to each action the agent does by giving it a reward or a punishment, which might be financial gain. As such, the agent optimizes the decision-making policy from these experiences in an attempt to increase future rewards.

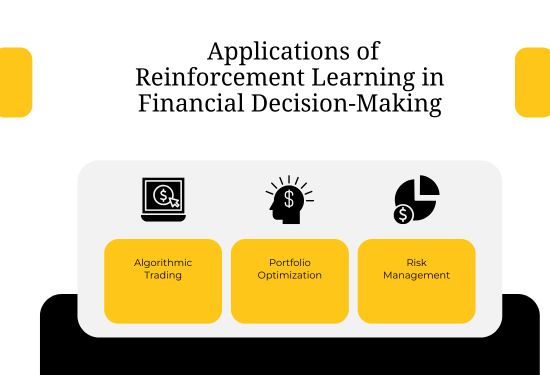

Key Applications of Reinforcement Learning in Financial Decision-Making

Algorithmic Trading

RL algorithms are more widely used in algorithmic trading, which tries to make transactions at a favorable time. Since RL is based on analysis of historical data and current market conditions, RL agents can find promising trades and modify the algorithms as soon as the markets alter. For instance, advanced techniques, such as Deep Q-Networks (DQNs), enable the model to analyze large volumes of information and create trading approaches to increase the profitability of trades.

Portfolio Optimization

In managing a portfolio, RL is used to cure the implication of separating the risk from the return through the flexibility of the investment. In contrast to the conventional approaches that rely on set assumptions, the RL algorithms find out the changes in the marketplace and adjust the portfolio’s risk or return accordingly. Therefore, other advanced techniques, such as Proximal Policy Optimization (PPO) or Actor-Critic methods, are applied in RL-driven portfolio management to enhance such decisions.

Risk Management

Financial markets are always complex and unpredictable, requiring comprehensive risk management. Reinforcement learning (RL) may help determine potentially risky market trends and construct models that enable the prevention of potential losses. By informing what actions will lead toward a positive outcome, RL models aid decision-making in financial institutions by mitigating market risks.

Market Simulation and Scenario Analysis:

RL models are also valuable for simulating various market scenarios and stress-testing investment strategies. By training on different market conditions—such as bull, bear, or volatile phases—RL systems can identify strategies that hold up across diverse situations. This predictive capability is particularly beneficial for financial institutions that need to ensure the robustness of their strategies under different conditions.

Benefits and Challenges of Reinforcement Studying finance

Additionally, RL models may be utilized to analyze various market circumstances and assess the efficacy of specific tactics. Therefore, training RL systems on various market conditions allows the system to learn good strategies that perform well under different conditions. For financial organizations, this predictive ability is highly significant as it can evaluate the strategy's decision-making in various circumstances.

Predicting Market Trends with AI: How Accurate Are These Tools?

Creative Strategies for Small Business Owners

Inflation’s Impact on Everyday Life

Online Financial Planning Services for Seniors

Funds, Bonds, Stocks: Knowing the Differences

Credit Cards: Mastering the Perks Game

Personal Bankruptcy: What We Need to Know