Is it possible to turn a monthly savings of only $200 into a down payment for a house after ten years? For wealthy people used to dealing with big investments, the thought of growing their money with such small contributions may sound unrealistic. Yet, the power of compound interest proves otherwise, showing that steady, small savings can lead to significant growth over the years.

The Mechanics of Compound Interest: More Than Just Growth

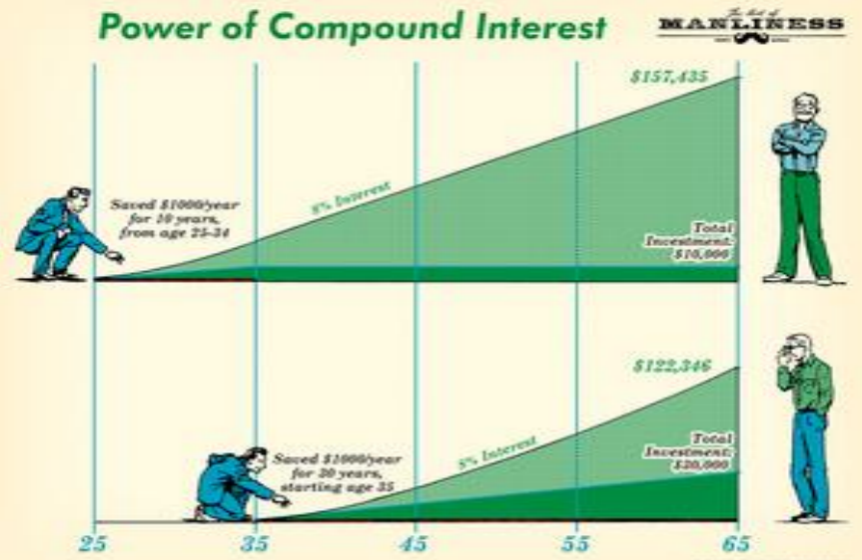

Compound interest is not just about getting interest on your initial amount; it's about how much it can grow exponentially when you reinvest the interest earned. In contrast to simple interest, which only adds to the original sum, compound interest earns returns on both the initial investment and any interest that has already been added. For example, if you save $200 each month with an annual interest rate of 6%, in the first month, the $200 will start to earn interest. In the second month, the interest gained during the first month is combined with the principal amount, allowing this increased total to start generating interest too.This process repeats 120 times over ten years, creating a snowball effect.

Advanced financial models reveal that by investing $200 every month at a 6% annual return, you would accumulate about $31,000 in ten years. However, the real benefits appear when the interest rate increases. With an 8% return, the same monthly investment could grow to around $36,000. This shows that even slight changes in interest rates can lead to major differences in returns over the long run, underscoring why selecting the right investment options is crucial.

Leveraging High - Yield Opportunities

Wealthy individuals have unique investment opportunities that can greatly enhance the compounding effect. Rather than relying on standard savings accounts that yield very little, they can choose alternative investments such as exchange-traded funds (ETFs) that focus on stocks that pay dividends, which tend to deliver greater returns. Typically, dividend-focused ETFs yield between 3% and 5%, with some even exceeding 6% in strong market conditions. These funds gather money from various investors to create a diverse range of stocks that consistently pay dividends. By reinvesting these dividends, investors can boost their compounding growth, speeding up their wealth accumulation.

Peer-to-peer lending platforms present an alternative choice. These services connect borrowers and lenders directly, removing the role of traditional financial intermediaries. While investments made through these platforms involve greater risks, they may provide annual returns between 8% and 12%. By diversifying investments across different loans and borrowers, investors can reduce risk while benefiting from enticing interest rates, thereby enhancing the compounding effect on their savings each month.

The Role of Time and Consistency

The key element in the equation of compound interest is time. By beginning to save sooner, individuals allow their money more opportunities to grow. Even those with substantial disposable income can benefit from starting with small amounts and maintaining their savings over time, as this can build a financial cushion or aid in achieving major future expenses like buying a home. Staying consistent also involves avoiding the temptation to take out money early. Each withdrawal interrupts the compounding process, which can lead to losing thousands of dollars in potential growth in the long run.Additionally, the mental benefits of regularly saving small amounts should not be ignored. It fosters a sense of financial responsibility, which can help when dealing with larger investments. For wealthy individuals, this habit serves as a reminder of the importance of every dollar and highlights the necessity for careful, long-term planning to safeguard and grow their wealth.

From Savings to a Down Payment

Although a sum between $30,000 and $36,000 may not fully pay for a home, it can represent a significant down payment, particularly in regions where property prices are lower or for houses that are not overly expensive. Typically, many areas require a down payment of 10% to 20% to obtain a mortgage. Making a $30,000 down payment on a $300,000 property can lead to notably lower monthly payments and reduced interest expenses throughout the mortgage term.Furthermore, the savings discipline and financial understanding gained from this process can be beneficial for investing on a larger scale. Wealthy individuals may leverage this experience to delve into more intricate investment approaches, augmenting their financial portfolios even further.

In summary, the notion that saving $200 each month could result in buying a house within ten years is not unrealistic. Due to the effects of compound interest, smart investment decisions, and steady commitment, even small monthly savings can become a valuable financial resource. For wealthy individuals, this idea underscores the significance of making thoughtful financial choices, no matter how trivial they may seem.

Picking & Using Your First Credit Card Wisely

Global Inflation Trends: Why Certain Economies Are More Affected Than Others

Investing in Private Debt: An Emerging Asset Class

Overseas Property: Profitable Reality Check

Global Asset Allocation: A Beginner's Guide

Overseas Returnees' Financial Reset: Seizing Cross - Border Allocation Windows

Apply for bankruptcy, then I have nothing?